What’s in a Name? Trump Account, Baby Bond, Whatever… Saving Young Matters

October 14, 2025

When the One Big Beautiful Bill Act (OBBBA) was signed into law July 4, 2025, it introduced a new type of savings program for children. While informally referred to in some media as “Trump Accounts,” it’s important to focus on the program’s structure and potential benefits, rather than nickname.

If you, a friend, or a family member recently had a child — or is expecting — this new savings vehicle may be worth considering. Even if this vehicle isn’t relevant to your situation, one of its key attributes — harnessing the power of saving early — provides a good reminder for us all.

New Savings Program Overview

Highlights of the new Trump Accounts program include:

- Automatic $1,000 government seed deposit for children born between January 1, 2025, and December 31, 2028, provided they are U.S. citizens with a Social Security number.

- Annual contributions of up to $5,000 by family members (and up to $2,500 by employers, in some cases), invested in a low‑cost U.S. stock index fund, with tax‑deferred growth.

- No withdrawals allowed until the child reaches age 18, at which point the account transitions into a traditional IRA–like structure.

- The account can be used for qualified expenses such as education, first-home purchases, or launching a small business. Unrestricted withdrawals before age 59-½ may incur ordinary income taxes and a 10% penalty.

Some people have criticized the program, pointing to potential downsides, such as:

- Complexity

- Limited flexibility

- The fact that there are already robust alternatives, like 529 plans, that offer broader utility and higher contribution thresholds

- Concern about additional savings vehicles cluttering the financial landscape

Saving Early Is Financially Powerful

The core idea behind early‑childhood savings — regardless of the vehicle — rests on this timeless principle: compounding.

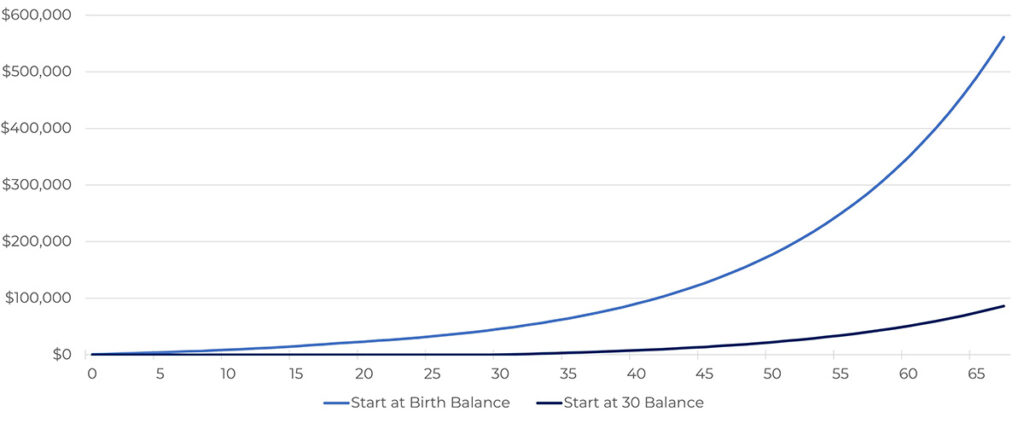

A modest seed and consistent annual contributions can multiply dramatically over decades thanks to compound interest. As an example, the following illustration assumes:

- $1,000 is deposited at birth

- $500 is contributed each year until age 18

- The account grows at 7%

Important Note: This is a hypothetical example for illustrative purposes only. It does not represent any specific investment product or guarantee of future results. Actual performance may vary.

Starting Early vs. At Age 30

As you can see, this modest savings plan can snowball into more than $500,000 by retirement, whereas starting at age 30 means you’ll be lucky to hit $80,000. Ouch.

Even if you did nothing but earn 5% on the $1,000 seed, it’d still double to about $2,400 by age 18.

Compounding doesn’t just work — it works hard.

Saving Early Is Emotionally Powerful

Research on children’s savings accounts has shown that even modest savings can positively influence academic outcomes and future financial behaviors. Kids with some form of designated savings, even as little as $1 to $499, are more than four times as likely to graduate from college than those without any savings.

Embedding saving and investment behaviors early on, even in a small way, can help children build financial confidence, set expectations around long-term planning, and introduce them to the principles of investing and asset accumulation.

Suggestions for Early-Age Savings Accounts

If you’re inspired by the concept of early savings, here are some things to consider:

- Explore a variety of available tools — 529 plans, Coverdell ESAs, and custodial accounts — to start a savings habit today.

- Teach kids early about investing, compounding, and setting financial goals.

- Use windfalls wisely. Gift checks, birthday money, or the like can be fun “early savings projects” with lasting impact.

- Think long-term. The reason financial advisors recommend you start planning for retirement in your 20s is the same reason starting at birth can be transformative.

Bottom line: It doesn’t matter whether it’s dubbed a Trump Account, a baby bond, or a children’s savings account. The real advantage lies in harnessing time and compounding, launching a savings mindset early, and giving the next generation a tangible stake in their financial future

Sourcing: doi.org/10.1016/j.childyouth.2012.12.003, “Small-dollar children’s savings accounts and children’s college outcomes by income level,” 12/27/2012

Let's Talk

If you’d like to discuss what savings vehicles are best for you and your family